This is the reproduction of an article in IFR Asia magazine.

In the face of formidable uncertainties this year, investors may still seek the comfort of fixed income, says Dilip Parameswaran

Despite all the misgivings at the beginning, last year turned out to be a good one for fixed-income investors. Asian dollar bonds ended the year with a return of 5.8%, composed of 4.5% for investment-grade and 11.2% for high-yield bonds, according to JP Morgan Asia Credit Index data. We are beginning another year full of uncertainties. What does 2017 hold in store for fixed-income investors?

The first big uncertainty relates to the path of US interest rates. The Fed has begun raising rates and has signalled that three rate increases are in the offing this year and three more next year. A sustained period of job growth has brought US unemployment down to 4.7%, but more importantly the pace of wage increases to 2.9% per year. While these numbers underpin the Fed’s planned rate increases, the key unknown is the impact on any potential fiscal stimulus on growth and inflation.

That brings us to the second key uncertainty: the Trump administration’s plans for the economy. It is widely understood that the next administration intends to provide fiscal support through a cut in taxes and an increase in infrastructure spending, but the extent of the stimulus and its potential impact are unknown. If these plans start nudging inflation up to a level higher than the Fed’s current expectations, the Fed might have to respond by raising rates faster.

Another unknown is the extent to which the Trump administration’s policies on trade and the dollar will influence key economic variables. Mr Trump has espoused various protectionist views and may tolerate a weaker dollar. While a weaker currency might push inflation higher, the final impact of protectionist trade policies, particularly on growth and employment, is uncertain.

China is the other piece in this moving puzzle. At the beginning of last year, worries about China’s economy dominated the markets, but as time went on, growth began to stabilise and greater uncertainties – including the US presidential election – took over. This year too, the markets are resting on the comfortable assumption that China would manage growth of about 6.5%.

But China still faces a myriad of economic issues, all of them carried over from the last year. While economic growth last year was propped up by continued flow of credit to the economy, the total debt in the system has reached close to 300% of GDP, according to various estimates. China also faces the challenge of rising capital outflows in response to slowing growth and a depreciating currency. While property construction was a key support for the economy last year, property prices in many cities have risen to such unsustainable levels as to prompt a round of regulatory constraints. The government may provide a measure of support to the economy through an expanded fiscal deficit, but it would exacerbate the challenge of managing the total debt in the economy. On top of all these domestic economic issues, there is the added challenge of a strained trade and political relationship with the US. China may yet emerge as one of the key trouble spots this year.

Where does all this leave the fixed-income investor in Asia? We believe that Asian dollar bonds could again produce positive returns of 2%-3%, without leverage.

One key driver of the returns is, of course, US Treasury yields. Based on the current expectations for the Fed rates, we believe the 10-year yields could rise by about 50bp over the year to reach close to 3%.

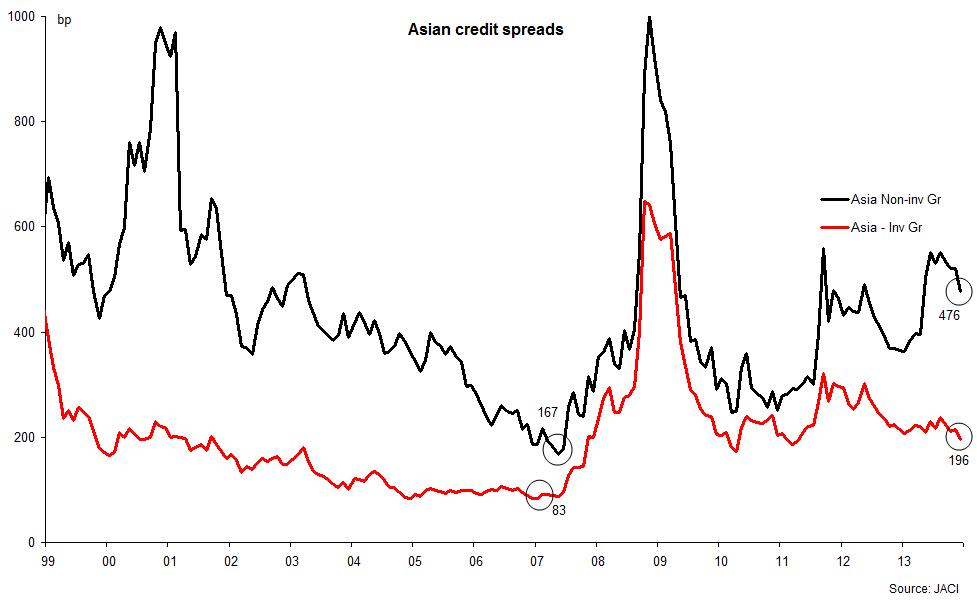

The spreads on Asian dollar bonds narrowed by about 25bp last year for investment-grade and 130bp for high-yield bonds, according to the JACI data. This year, we expect investment-grade spreads to finish flat and high-yields bonds to widen by 50-75bp. This is primarily because the positive performance last year has left Asian spreads somewhat tight by historical standards and in comparison with US spreads.

Credit defaults are unlikely to turn into a big issue for Asian bonds. Moody’s expects that, after a temporary pick-up in the early part of the year, the global high-yield default rate will edge down from 4.4% to 3% over the year. In Asia, defaults have always been episodic and not systematic. Given the prevalence of family ownership, government connections and bank support, Asian issuers have averted defaults in many difficult situations.

The technical factors for Asian bonds were strong last year. Nearly three-quarters of Asian bond issues were placed within Asia, up from 63% the year before. Support from Chinese investors in particular has been one of the contributing factors. We expect these factors to continue supporting the market this year as well.

While some market players expect a wholesale shift of funds to equities this year, the so-called “great rotation” has so far proved to be the wolf that never came. With major uncertainties confronting the economic world this year, investors might yet prefer the cosy comfort of fixed income for a while yet.

Despite all the misgivings at the beginning, last year turned out to be a good one for fixed-income investors. Asian dollar bonds ended the year with a return of 5.8%, composed of 4.5% for investment-grade and 11.2% for high-yield bonds, according to JP Morgan Asia Credit Index data. We are beginning another year full of uncertainties. What does 2017 hold in store for fixed-income investors?

The first big uncertainty relates to the path of US interest rates. The Fed has begun raising rates and has signalled that three rate increases are in the offing this year and three more next year. A sustained period of job growth has brought US unemployment down to 4.7%, but more importantly the pace of wage increases to 2.9% per year. While these numbers underpin the Fed’s planned rate increases, the key unknown is the impact on any potential fiscal stimulus on growth and inflation.

That brings us to the second key uncertainty: the Trump administration’s plans for the economy. It is widely understood that the next administration intends to provide fiscal support through a cut in taxes and an increase in infrastructure spending, but the extent of the stimulus and its potential impact are unknown. If these plans start nudging inflation up to a level higher than the Fed’s current expectations, the Fed might have to respond by raising rates faster.

Another unknown is the extent to which the Trump administration’s policies on trade and the dollar will influence key economic variables. Mr Trump has espoused various protectionist views and may tolerate a weaker dollar. While a weaker currency might push inflation higher, the final impact of protectionist trade policies, particularly on growth and employment, is uncertain.

China is the other piece in this moving puzzle. At the beginning of last year, worries about China’s economy dominated the markets, but as time went on, growth began to stabilise and greater uncertainties – including the US presidential election – took over. This year too, the markets are resting on the comfortable assumption that China would manage growth of about 6.5%.

But China still faces a myriad of economic issues, all of them carried over from the last year. While economic growth last year was propped up by continued flow of credit to the economy, the total debt in the system has reached close to 300% of GDP, according to various estimates. China also faces the challenge of rising capital outflows in response to slowing growth and a depreciating currency. While property construction was a key support for the economy last year, property prices in many cities have risen to such unsustainable levels as to prompt a round of regulatory constraints. The government may provide a measure of support to the economy through an expanded fiscal deficit, but it would exacerbate the challenge of managing the total debt in the economy. On top of all these domestic economic issues, there is the added challenge of a strained trade and political relationship with the US. China may yet emerge as one of the key trouble spots this year.

Where does all this leave the fixed-income investor in Asia? We believe that Asian dollar bonds could again produce positive returns of 2%-3%, without leverage.

One key driver of the returns is, of course, US Treasury yields. Based on the current expectations for the Fed rates, we believe the 10-year yields could rise by about 50bp over the year to reach close to 3%.

The spreads on Asian dollar bonds narrowed by about 25bp last year for investment-grade and 130bp for high-yield bonds, according to the JACI data. This year, we expect investment-grade spreads to finish flat and high-yields bonds to widen by 50-75bp. This is primarily because the positive performance last year has left Asian spreads somewhat tight by historical standards and in comparison with US spreads.

Credit defaults are unlikely to turn into a big issue for Asian bonds. Moody’s expects that, after a temporary pick-up in the early part of the year, the global high-yield default rate will edge down from 4.4% to 3% over the year. In Asia, defaults have always been episodic and not systematic. Given the prevalence of family ownership, government connections and bank support, Asian issuers have averted defaults in many difficult situations.

The technical factors for Asian bonds were strong last year. Nearly three-quarters of Asian bond issues were placed within Asia, up from 63% the year before. Support from Chinese investors in particular has been one of the contributing factors. We expect these factors to continue supporting the market this year as well.

While some market players expect a wholesale shift of funds to equities this year, the so-called “great rotation” has so far proved to be the wolf that never came. With major uncertainties confronting the economic world this year, investors might yet prefer the cosy comfort of fixed income for a while yet.

RSS Feed

RSS Feed